On the campaign trail in 2024, Donald Trump recognized that Americans were still deeply concerned about inflation and the cost of living, despite the improving conditions after the 2022 spike. To that end, the Republican candidate focused heavily on the issue and made all kinds of bold promises about “Day One” improvements, all while struggling with the most basic of questions: What would he actually do on the issue?

When pressed, he tended to focus on gas prices. To hear Trump tell it, he would focus obsessively on drilling for oil, everywhere and all of the time, which he said would lower gas prices, which in turn would make it more affordable to transport goods to marketplaces, which in turn would lower prices.

It was, to be sure, a highly dubious pitch rooted in suspect assumptions, but it was a line much of the electorate was willing to embrace, as evidenced by his return to power.

The gap between what Trump promised to deliver and what he has delivered is enormous — and growing. As The New York Times summarized, “Oil prices surged on Monday in a sign of growing concern that the war in the Middle East will continue to take a toll on energy supplies, raising gas prices for American consumers and weighing on the stock market.”

The Washington Post added, “The average cost of a gallon of regular gasoline in the U.S. increased by 34 cents in the last week to $3.32 on Friday, according to AAA. The cost of diesel has grown even more significantly and analysts expect the price of both fuels to keep climbing.”

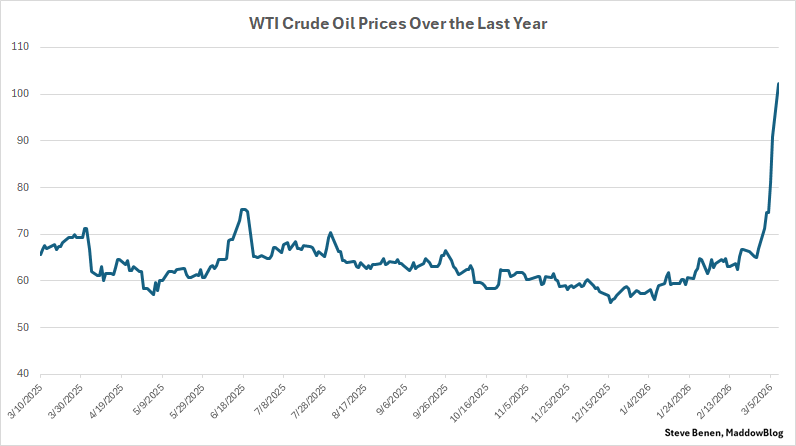

Broadly speaking, the benchmark metric eyed by the energy sector is West Texas Intermediate, which surged last week in ways unseen in years. (There’s also the Brent crude metric, eyed by international markets, which climbed at a similar pace.)

To put the increase in perspective, I put together this chart showing WTI prices over the last year.

To be sure, the White House has insisted that this is a temporary setback. In an item published to his social media platform on Sunday afternoon, the president argued after his latest golf outing, “Short term oil prices, which will drop rapidly when the destruction of the Iran nuclear threat is over, is a very small price to pay for U.S.A., and World, Safety and Peace. ONLY FOOLS WOULD THINK DIFFERENTLY!” (He was referring to an Iranian nuclear threat that he has claimed to have “obliterated” last summer.)

Time will tell just how long the higher prices will last and the extent to which the hike will reverberate throughout the global economy. But in the meantime, I find myself stuck on one nagging detail.

On Thursday afternoon, at a White House event intended to honor a championship soccer term, Trump took a moment to comment on an issue on the minds of many.

“Yesterday, my administration announced decisive action to help keep down the oil prices,” he declared. Moments later, he went on to say that oil prices “have pretty much stabilized.”

Right around the time Trump made those comments, oil prices were roughly $80 a barrel. They topped $100 soon after.

So here are the questions for the communications team in the West Wing: (1) Was the administration’s “decisive action to help keep down the oil prices” a failure? (2) Does the president know what “stabilized” means?

This post updates our related earlier coverage.